History of Russo-Ukrainian Gas Relations

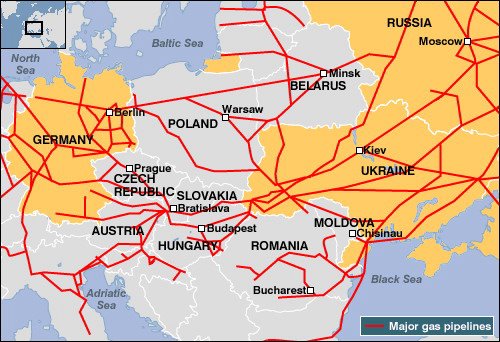

Ukraine is a major consumer of gas – consuming in the region of 70 bcm per annum,only around 20 of which are produced domestically. Ukraine relies on Russian import to satisfy the majority of its gas needs,thus creating a strong dependence. This situation is counterbalanced by Ukraine being a corridor for transit of about 80% of the total Russian gas exports to its European customers. The other 20% of Russian gas goes to Europe through Belarus.

The pipelines in the Soviet Union times have been built through Ukraine with an assumption that Russia and Ukraine will both collaborate within this framework indefinitely. However,in post-Soviet times the situation has changed,thus creating grounds for disputes between the countries.

In an attempt to manage the situation,Gazprom and Russian government adopted the following tactics since the late 1990s:

- Encouraged Turkmenistan to sell gas to Ukraine,thus allowing for larger transit deliveries of Russian gas to Europe;

- Creation of a string of intermediary trading companies to oversee transport and sometimes supply the gas to Ukraine. The following companies have been used:Itera (1998-2003),Eural Trans Gas (2003-2005) and RosUkrEnergo (RUE) (2005-early 2009).

Since 2002,a steady rise in world oil prices and European gas prices has been observed,thus increasing the differential between the European prices and those charged to CIS countries. From 2004 onwards,Gazprom called on CIS prices to be raised to the level of European netback (European border prices less transportation charges).

The first major dispute over price and terms on which gas was imported developed in January 2006,resulting in Russia cutting off Ukrainian import volumes for three days. Ukraine responded by diverting some gas destined for Europe,thus reducing supply. The conflict was resolved and Gazprom has not been able to negotiate the European netback prices with Ukraine on this occasion,because Ukrainian government and Naftohaz Ukrayiny showed they would not hesitate using their transit levers as a bargaining power.

In September 2007,Yulia Timoshenko (returning Prime Minister) promised to eliminate RosUkrEnergo from the gas trade intermediary position as well as Ukrhaz-Energo (a vehicle,which ensured RUE’s strong position in Ukrainian gas market).

The next step in setting out the type of Russo-Ukrainian gas relations was a memorandum between the countries’ governments signed by Prime ministers Putin and Timoshenko followed by an agreement On the Principles of Long-term Cooperation in the Gas Sector signed in late 2008 by Aleksey Miller and Oleg Dubyna,Gazprom and Naftohaz CEOs. The main articles of these documents were:

- From 1 January 2009,Naftohaz would become sole importer and would buy gas directly from Gazprom,while Naftohaz debts to RUE would be converted into debts to Gazprom (meaning that both RUE and Ukrhaz-Energo would no longer be involved in gas import);

- Import prices and tariffs to be raised step by step to “market,economically based and mutually agreed levels” within three years (subject to further negotiations);

- Gazprom and Naftohaz would jointly export some gas to Europe (an unprecedented term).

Neither of these two documents specifies the role of RUE in sales of central Asian gas in central Europe. According to Mr Firtash (a co-owner of RUE),the company intends to supply 7 bcm of gas to Poland,Hungary and Romania in 2009.

Naftohaz was due to pay its debts to Gazprom before a new contract could be signed but it failed to do so.

On the 1st of January 2009,Gazprom cut all supplies to Ukrainian consumers but continued to pump the gas for Europe. Following a confusing situation with the transit gas,Russia cut off all gas supplies on the 7th of January and European consumers remained without imported gas for two weeks until the conflict between Russia and Ukraine was finally resolved.

Ukraine and Russia signed two new contracts covering 2009-2019 – for supply and Transit of Russian gas. Both contracts are quite complex,but the main provisions are as follows:

Supply contract

- 40 bcm of gas to be delivered to Ukraine in 2009 and 52 bcm annually from 2010 onwards;

- Prices are set at 80% of a European price in 2009 and full European price from 2010 onwards (this price will change quarterly and was $360/mcm for the first quarter of 2009);

- Strict rules on taking extra gas (serious penalties in case of taking over the agreed limit) and strict payment terms for Naftohaz Ukrainy,whereby it is required to pay monthly for 100% of gas delivered by the 7th day of the next month;

- Gazprom will sell gas directly to Naftohaz on Ukraine’s borders with Russia and Belarus,thus eliminating RUE as an intermediary;

- Gazprom-Sbyt,Gazprom’s wholly-owned trading subsidiary,will be responsible for marketing at least 25% of the imported gas (which is 10 bcm in 2009 and 13 bcm/annum from 2010 onwards.

Transit contract

- The annual transit volume of at least 110 bcm (120.083 bcm in 2009);

- The transit tariff set at $1.7/mcm/00km in 2009. From 2010,the tariff will be $2.04/mcm/00km plus an element based on 2009 prices;a similar formula will be used onwards;

- $1.7bn advance payment for transit services to be made by Gazprom intended for repayment of legal claims on RUE transferred to Naftohaz by Gazprom.

There have not been any disruptions to gas supply since the beginning of 2009,as Ukraine has met its payment obligations to Russia,but there is still tension with regards to this issue. Should Ukraine default on its payment and Russia decide to cut off gas supplies to Ukraine again,Ukraine will most likely respond as before – by stopping transit to the European consumers. Instability in relationship between Russia and Ukraine causes disturbances for the EU countries worried to find themselves without gas caught up in Russo-Ukrainian disputes again.